This section of the Subaru Accounting Manual deals with the following subjects related to expenses:

Expense Classification

Profit Center Concept

Methods of Distribution or Allocation

Expense Classification

All operating expenses on the Subaru Financial Statement are broken down into four categories – Selling, Personnel, Operating, and Overhead. Within the subcategories are individual expense classifications. There are other accounts that represent expenses but do not fall into the category of operating expenses. These are described as Deductions From Income.

A diagram of this structure would look like this:

Selling (Variable) Expense

Personnel Expense

Operating (Semi-Fixed) Expense

Overhead (Fixed) Expense

Within the subcategories are individual expense classifications. For example, the expense classifications under Personnel Expense are:

Salaries - Owners

Salaries - Supervision

Compensation - Advisors, Wholesale, Counter

Compensation – Express Service

Salaries - Clerical

Other Salaries & Wages

Taxes - Payroll

Employee Benefits / Pension Fund

Absentee Compensation

The total of the balances in these classifications will equal Total Personnel Expense.

A question that often arises is “what is the logic behind the expense classification between Variable and Fixed Expenses?” The answer is that each subcategory has a direct relationship to sales volume. To use the two extremes as examples:

Variable Selling Expense consists of expenses that vary in an almost direct relationship with sales volume. As sales volume increases, variable selling expense will increase in an almost directly proportional manner.

Fixed Expense represents an expense group that will move up or down very little and bear very little relationship to changes in sales volume.

The following is a description of the subcategories and their expected relationship to sales volume:

Variable Selling Expense will change in relationship to sales on a monthly basis.

Personnel Expense changes very little in its relationship to Sales. Personnel Expense tends to change based on:

Pay increases

The need to increase or decrease the number of employees because of significant changes in sales volume.

The relationship between Operating, or Semi-Fixed Expense and Sales will appear relatively indirect. For example, a gradual increase in sales may lead to a need to make a larger investment in Telecommunications devices but will not cause proportional short term changes.

Overhead, or Fixed Expense varies within a very narrow range and shows virtually no direct relationship to Sales. Sales pressure may cause a sudden change in Fixed Expense (for example, the addition of a used car facility or storage lot) but subsequent Fixed Expense levels and changes in Sales will show very little relationship.

The profit center concept states that all expenses other than Deductions From Income benefit the operating departments. Operating expenses include expenses that can be attributed to a specific department as well as expenses that are assigned to the operating departments using an allocation formula.

Most of the expenses allocated to a department are expenses over which the department manager has some control. There are other allocated expenses over which a manager has little control, but from which their department does gain some benefit. For example, the sales manager has little control over rent expense, but his/her department does gain a benefit from that expense: a facility from which to sell cars.

The objectives of the profit center concept are threefold:

To give managers a more realistic view of overall dealership operations.

To help managers gain a greater awareness of the true cost of operating the business and each department.

To help managers develop departmental goals that are more closely aligned with total dealership goals.

The method of allocating an expense depends upon three things:

Type of expense.

How the benefit of that expense is received by the departments.

Degree of distribution accuracy in relationship to allocation formula complexity.

It is preferable to have an acceptable level of accuracy based on a simple, easily understood allocation formula rather than a very high level of accuracy based on a complex allocation formula.

As discussed in the previous section, any expenses that can be associated with a specific user department should be charged directly to that department.

Allocation formulas should be reviewed at the beginning of the year and adjustments made where appropriate. Once allocation formulas are established for the year, they should be reviewed quarterly or mid-year for adjustment.

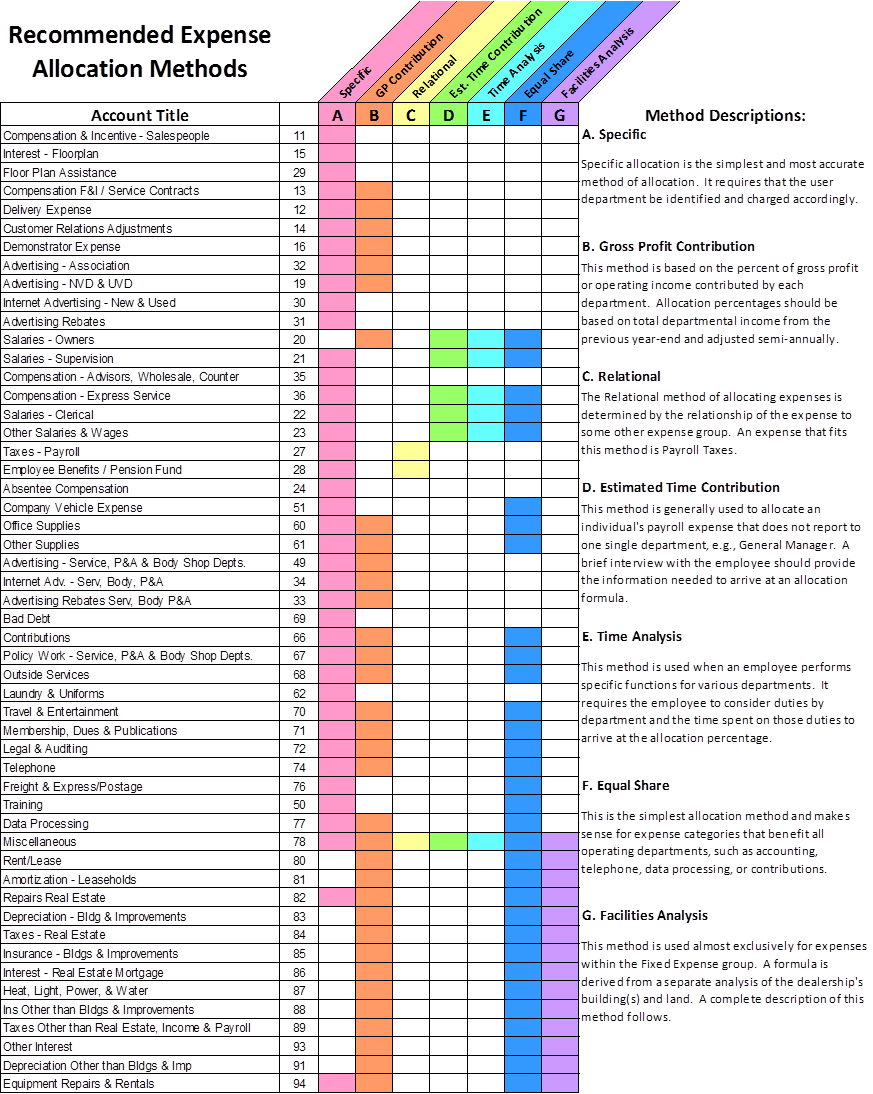

The chart on the prior page summarizes recommended expense allocation methods by account category. The following pages describe each expense allocation method in detail.

A. Specific

Specific allocation is the simplest and most accurate method of allocation. This method requires a document, usually an invoice from a vendor, to identify the user department. The signature of the Manager of the user department should appear on the purchase order or the invoice.

The type of goods or services purchased, in addition to the name of the Manager approving the purchase, usually provides the necessary information to identify the department to be charged. For example, gas for the parts delivery truck will be charged to the Parts Department based on the goods purchased and the signature of the Parts Manager.

B. Gross Profit or Operating Income Contribution

This method of allocation is based on the percent contribution from each department. The following chart provides an example of allocation percentages derived from gross profit contribution.

Department Operating Income Contribution % of

New – Subaru Vehicles $570,000 29.8

New - Other $190,000 9.9

Used $290,000 15.2

Service $375,000 19.6

Body Shop $140,000 7.3

Parts $346,000 18.2

Total Operating Income $1,911,000 100.0

The allocation percentages for Gross Profit Contribution or Operating Income Contribution should be based on the gross profit or income for the previous year-end. This formula must be adjusted at the beginning of each year using the figures from the previous year-end Financial Statement. Again, an exception should be made where there is substantial change to the relationship of departmental contributions.

An example of an expense that might be appropriately allocated based on gross profit contribution would be Account 77, Data Processing Services. The idea is that the cost of software purchased to provide sales and invoicing systems for all operating departments warrants the use of a gross profit contribution allocation method because the benefit should be closely related to gross profit activities.

C. Relational

The Relational method of allocating expenses is determined by the relationship of the expense to be allocated to some other expense or group of expenses. An example of an expense that might fit this method of allocation is Payroll Taxes.

In this case, the amount of expense in each department for Personnel Expense Accounts and the productive labor in Service and Body Shop should provide an excellent basis for percentages to use in allocating Payroll Taxes. As in most of the other allocation methods, this relational allocation formula can be derived from the previous year’s Financial Statement. Once established, it should checked mid-year for necessary adjustments due to operational changes.

D. Estimated Time Contribution

In some cases, it is not possible to obtain a detailed analysis of the time contributed to each operating department by certain individuals in the dealership. Therefore, it becomes necessary to interview these individuals and determine their estimate of the relative amount of time spent in each operating department.

E. Time Analysis

This method of allocation is used when a dealership employee performs specific functions for various departments on a regular basis. This requires the employee to consider responsibilities and duties as they relate to each department. The result is a determination as to the percentage of compensation to be charged to each department. An example would be wages for Lot Attendants and Drivers.

F. Equal Share

This is a very simple allocation method that is usable only for expense accounts that generate relatively small monthly totals that are not easily identifiable as pertaining to a specific department or departments. Simply divide the expense by the number of operating departments within the dealership and allocate an equal share of the expense to each department. An expense that might be appropriately allocated using this method is Contributions.

Note: The Subaru Financial statement provides for the allocation of personnel in the Personnel Summary section on Page 4. The method used to allocate personnel in this section should be consistent with the expense allocation method. For example, if the owner’s salary is divided equally between Departments New, Used, Service and Parts the personnel count for the owner should indicate .25 in each of the four departments.

G. Facilities Analysis

The Facilities Analysis allocation method is used almost exclusively on expenses within the Fixed Expense group. The development of the Facilities Analysis formula requires some time and attention to detail. The formula is derived from analyzing the dealership’s building and land separately. The information from the two analyses is then combined to arrive at allocation percentages for Fixed Expenses.

Buildings

Determine the square footage of the building space occupied by each department and calculate the allocated building costs using weighted value.

The total cost of dealership facilities must be broken down between land and buildings. In the event the facilities are rented or leased, assume that the monthly rent or lease payment represents 1 1/4% of cost. For example, a $28,750 per month rent would translate to a total facilities cost of $2,300,000 ($28,750 ÷ 1 1/4%).

Another method is to take the cost of buildings and land from the property tax assessment notices. In most cases, the assessment notices will provide an assessment value breakdown between land and buildings/improvements. If this information is not available on your tax assessment notice, an appraisal can usually be obtained from a professional appraiser.

Determine the square footage of buildings occupied by each operating department. Do this for land and buildings separately.

Measure off the building space occupied by each operating department. This can be done from blueprints or floor plans if they are available. Do not bother to measure space occupied by non-operating departments.

List the square footage as shown in Chart 1, Allocated Building Costs Using Weighted Values. The weighting factors shown in the chart are based on relative construction costs. Multiply the square footage for each department times the weighting factor to arrive at the weighted value for each department.

Use the weighted values to determine the percentage to use in arriving at the building costs to be allocated to each department.

Multiply the percent derived times total building costs to determine assigned $ value for each department

Land

Determine the square footage of the land area used by each operating department and calculate the allocated land costs using weighted values.

The total cost of dealership facilities must be broken down between land and buildings. In the event the facilities are rented or leased, assume that the monthly rent or lease payment represents 1 1/4% of cost. For example, a $28,750 per month rent would translate to a total facilities cost of $2,300,000 ($28,750 ÷ 1 1/4%).

Another method is to take the cost of buildings and land from the property tax assessment notice. In most cases, the assessment notice will provide an assessment value breakdown between land and building/improvements. If this information is not available on your tax assessment notice, an appraisal can usually be obtained from a professional appraiser.

Determine the square footage of land used by each operating department. Do this for land and buildings separately.

Measure off the land by each operating department. Use a plot plan if available. Be certain to include off-site storage facilities.

List the square footage as shown in Chart 2, Allocated Land Costs Using Weighted Values. The weighting factors shown in the chart are based on relative values of that portion of land traditionally used by each operating department.

The concept here is that business property exposed to traffic carries a greater value than property that has little or no traffic. Therefore, new and used car display areas will have a higher land value per square foot than will the body shop area.

Use the weighted values of the land used by each operating department to arrive at the percentages required to determine the assigned dollar values for each department. The assigned values for each department’s building and land use are then combined to arrive at the percentage to be used in allocating Fixed Expenses. This is demonstrated in Chart 3,Facilities Analysis: Fixed Expense Allocation Percentages Based On Assigned Building and Land Values.

The weighting factors used in the examples are based on national information. If you feel that the construction costs and relative land values are considerably different in your geographical region, you can adopt local information to develop your own weighting values.

|

Allocated Building Costs |

|||||

|

Using Weighted Values |

|||||

|

|

|

|

|

|

|

|

|

Actual |

Weighting |

Weighted |

% Based on |

Assigned |

|

Department |

Square Feet |

Factor |

Value |

Weighted Value |

$ Value |

|

New Subaru |

2,700 |

2 |

5,400 |

17.0 |

255,000 |

|

New Other |

|

|

|

|

|

|

Used |

350 |

2 |

700 |

2.2 |

33,000 |

|

Service |

10,100 |

1.5 |

15,150 |

47.6 |

714,000 |

|

Body Shop |

5,400 |

.8* |

4,320 |

13.6 |

204,000 |

|

Parts |

6,250 |

1 |

6,250 |

19.6 |

294,000 |

|

Total |

24,800 |

|

31,820 |

100.0 |

1,500,000 |

|

|

|

|

|

|

|

|

* Body Shops with paint booths, heat dry booths and alignment racks should use a weighing factor of 1.5. |

|

||||

|

Chart 2 |

|||||

|

Allocated Land Costs |

|||||

|

Using Weighted Values |

|||||

|

|

|

|

|

|

|

|

|

Actual |

Weighting |

Weighted |

% Based on |

Assigned |

|

Department |

Square Feet |

Factor |

Value |

Weighted Value |

$ Value |

|

New Subaru Display |

10,000 |

2.0 |

20,000 |

|

|

|

Storage |

22,000 |

1.0 |

22000 |

|

|

|

Sub-Total |

32,000 |

|

42000 |

26.7 |

213,600 |

|

New Other |

|

|

|

|

|

|

Used Display |

21,000 |

2.5 |

53 |

|

|

|

Storage |

4,000 |

1.0 |

4,000 |

|

|

|

Sub-Total |

25,000 |

|

56,500 |

36.0 |

288,000 |

|

Service |

26,000 |

1.5 |

39,000 |

24.8 |

198,400 |

|

Body Shop |

7,000 |

1.2 |

8,400 |

5.3 |

42,400 |

|

Parts |

7,500 |

1.5 |

11,250 |

7.2 |

57,600 |

|

Total |

97,500 |

|

157,500 |

100.0 |

800,000 |

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||